Paris Pender

Head of PT and Macro Credit Trading, Trumid

A market protocol running steady

Portfolio Trading (PT) continues to be a market success story, with PT’s share of U.S. electronic corporate bond trading exceeding 21% in early 2025 vs. just 6% in 20211. The protocol has come of age, quickly evolving from new innovation to an essential tool for both buy-side participants and dealers.

What makes this success so evident?

- PT consistently delivers reliable liquidity, certainty of execution, and (often) tighter bid-offers, even in shifting market conditions.

- Trading and participation have increased, with asset managers relying on PT as a core execution tool and dealers scaling their infrastructure to support rising demand.

- Pricing remains competitive and transparent, enabling efficient clearing of both large and smaller lists.

At Trumid, portfolio trading remains a key growth driver. In 2025, Trumid PT Average Daily Volume grew approximately 50% year over year, significantly outpacing the 22% growth in TRACE™ PT volumes over the same period2. Trumid continues to demonstrate how technology-driven innovation is reshaping market behavior and setting new benchmarks for consistency and execution efficiency.

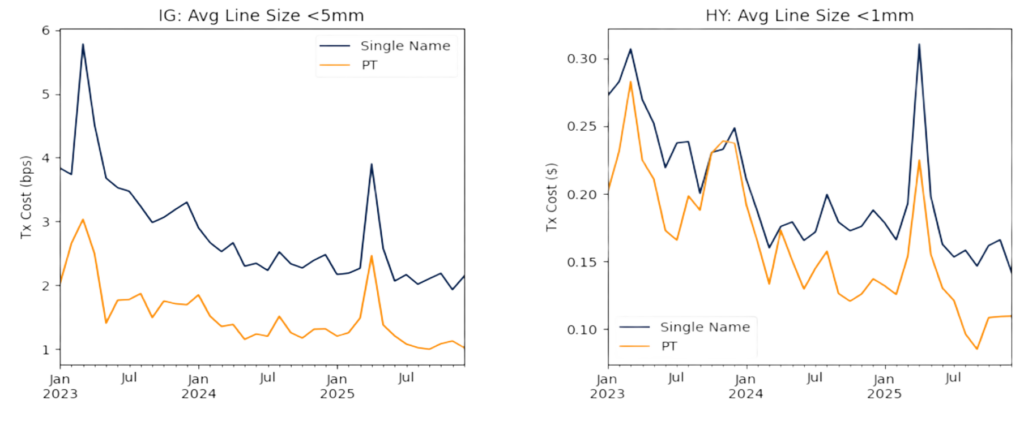

As PT’s expansion continues, it begs the question: What’s next for the market? As evidenced by the data in the graphs below, the protocol has become so efficient and pricing so competitive that the landscape seems ripe for evolution, perhaps to the point where continued evolution becomes more of a necessity than a possibility.

Average PT Bid-Offer vs. Market Volatility 2022–2025

Dealer engagement is evolving

PT’s story was defined by rapid expansion and differentiated value in 2023 and 2024, while 2025 was a year of refinement.

- Dealer participation is now broader than ever, with 20-25% of dealer-to-client volumes consistently traded via the protocol in 20253.

- Dealer engagement has also advanced, with more consistent quoting, tighter covers, and resilient performance during periods of volatility throughout 2025, particularly in April.

At the same time, as the protocol has matured, margins have compressed and balance sheets have ballooned, elevating the importance of efficiently recycling residual risk.

In principle, the ability for dealers to move residual risk quickly should lead to more competitive quotes on the follow and a virtuous circle of liquidity. However implementations of this concept have been problematic.

Trumid’s response has been to build a comprehensive ecosystem to help dealers and buy-side clients engage residual risk more efficiently. Dealers can post their residuals, clients can see them in the system, click to engage, and see inventory numbers tick down in real-time. This low-touch workflow can be screened by thousands of clients simultaneously against daily order blotters, fund compositions, or other interests.

Innovation will be the release valve

So what comes next? A helpful analogy may be one that comes up in AI conversations—the U.S. transformation from an agrarian to industrial economy. Even in 1900, agriculture accounted for 41% of jobs; by 2000, it was under 2%4. But rather than destroy humanity, automation has instead unlocked new opportunities, leading to careers that we couldn’t have imagined, like cloud engineer or TikTok influencer. None of us want to go back to life in 1900, just as no one in finance wants to retreat from technology that enables instant, low-cost execution.

My premise here may sound a bit contrarian, but I believe in our collective ingenuity. I expect pricing to go even tighter before the strain resolves. Numbers in comp will go up, covers will go down, and clients will continue to demand more and better value. And rather than retreat, the dealer collective will step up.

Pricing and risk management will also improve and collectively we’ll move towards a tighter but higher volume future. Boundaries will be pushed, and new paradigms will emerge. PT will meld better with the broader market and increase its overall efficiency.

I also believe in energy minimums, and I think we’re in one. Just like we’re not going back to the farm, we’re not going back to the margins of yesterday. While it’s natural to feel nostalgic for the 3pt bid offers on generic bonds in the 1980s, think of how much more the bond market supports today.

Lower costs, larger opportunities

The bottom line is that lower costs unlock larger opportunities. Traders at credit shops have long shared how they could implement a range of high-Sharpe strategies if transaction costs were lower. Maybe those days are approaching.

If margins don’t bounce back, perhaps volumes and the varieties of credit strategies will rise in their place. With analytics improving and technology at a tipping point, the asset class is poised for growth. When labor-intensive tasks become automated, new opportunities emerge, and if asset managers deploy new uncorrelated strategies, overall credit volumes and market interest should rise.

Ultimately this will benefit the true end users of credit: the borrowers, the investors, and the projects their debt funds. And I haven’t even mentioned ETFs and the ETF-ification of the fund world, the associated connection to PT, and the benefits it will bring.

Looking back, and ahead

In September 2024, we made three predictions for the evolution of portfolio trading in 2025:

- PT volumes would rise to 12–13% of the corporate bond market by year-end 2024, dip slightly in January, then continue to climb.

- PT would become 25% of market activity within three to five years, driven by deeper dealer commitment and a growing network effect.

- Technology for recycling dealer residual risk would advance, accelerating balance sheet turnover and enabling that growth path.

All three trends are now visible. PT volumes have hit 13% of TRACE™ volume, on track with our first prediction, and while they’ve retreated in recent months, external drivers and unexpectedly high issuance are a part of the story. The network effect continues to strengthen, with the majority of major dealers now quoting consistently and new participants filling niche roles5. Most encouraging of all, the third prediction has proven decisive: enhanced recycling technology and smarter redistribution have turned theoretical efficiency into observable liquidity benefits.

As we look ahead, it is clear that the next advances will not come from tighter spreads alone. Instead, they will come from improving the workflow itself, connecting data, analytics, and execution seamlessly.

Three predictions for 2026

- Portfolio trading will stabilize near 13–14% market share this year, as intra-month activity solidifies its role alongside traditional end-of-month flows.

- Dealer risk recycling will become an expected industry standard, establishing new efficiency metrics for balance sheet turnover.

- New market constructs will emerge, driven by analytics. New protocols, driven by maturing analytics, will form the base to advance volumes to their next plateau.

Closing note

Portfolio trading is no longer a novelty but a necessity. The real challenge now is how smartly the market evolves with its maturity. Efficiency isn’t the finish line; it’s the springboard for what comes next.

We’re excited about the innovation opportunities ahead and welcome your perspectives and collaboration. Connect with our Portfolio Trading team at team@trumid.com

Sources:

1. Crisil Coalition Greenwich, August Data Spotlight: U.S. Credit Trading. 2. Trumid internal data. 2024 vs. 2025. 3. Trumid, TRACE and other public data. 4. U.S. Labor Bureau of Statistics. 5. Trumid data.

© 2026 Trumid Holdings, LLC and its affiliates. All rights reserved. Trumid Financial, LLC is a broker dealer registered with the U.S. Securities and Exchange Commission (“SEC”) and is a member of FINRA and SIPC. Information included in this message does not constitute a trade confirmation or an offer or solicitation of an offer to buy/sell securities or any other products. There is no intention to offer products and services in countries or jurisdictions where such an offer would be unlawful under the relevant domestic law.